Obamacare still needs more young people to sign up. This will offset the high cost of the older, and probably less healthy people who are joining Obamacare plans. Oh, but then the White House has to coerce a sufficient number of thirty-somethings to join, too. Problem is, the health plans don’t make economic sense for many of these young adults.

So how costly are the Obamacare plans for young beneficiaries?

Forbes ran the numbers. Here are their results:

Overall, the Federal government reports that 32% of on-exchange enrollees as of March 1st are under the age of 34. And many of these are teenagers who are part of family policies, not the young folks that Obamacare is desperately targeting.

The final number of young enrollees falls well short of the required cohort. Premiums will rise next year to cover the adverse selection of older, and probably less healthy consumers.

So why are young adults staying away? Duh, it’s the economics.

Obamacare is asking young adults to subsidize the healthcare costs of older Americans. And Millennials are resisting this age-based transfer of wealth. Many are clearly opting instead to remain uninsured, or else they are buying cheaper health plans that don’t conform to Obamacare’s regulatory dictates.

They’re looking for affordable options like Direct Care. Somewhere where they know what they’re paying for and they know it will benefit them.

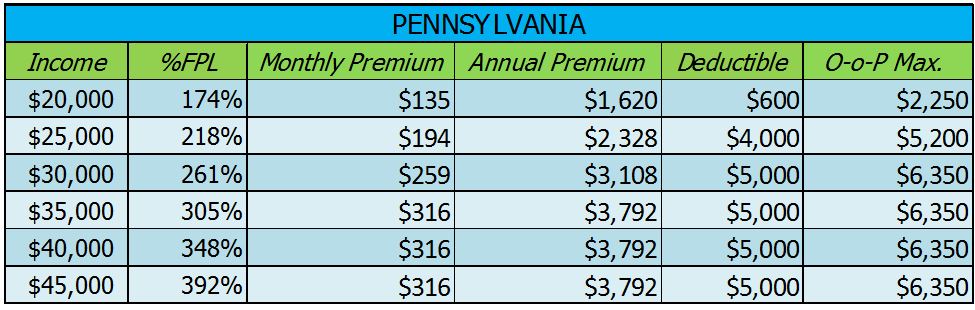

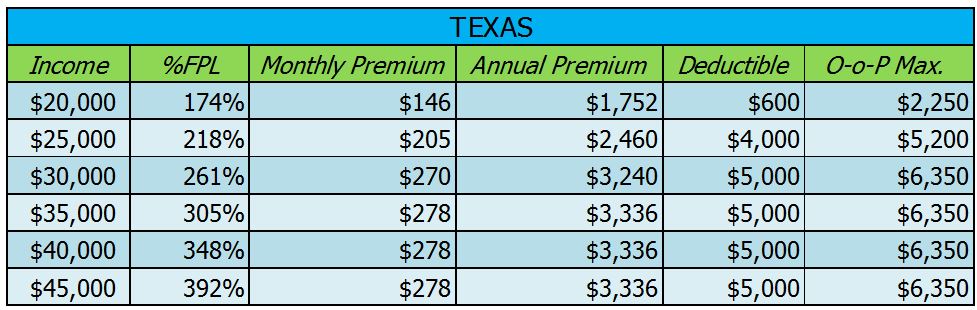

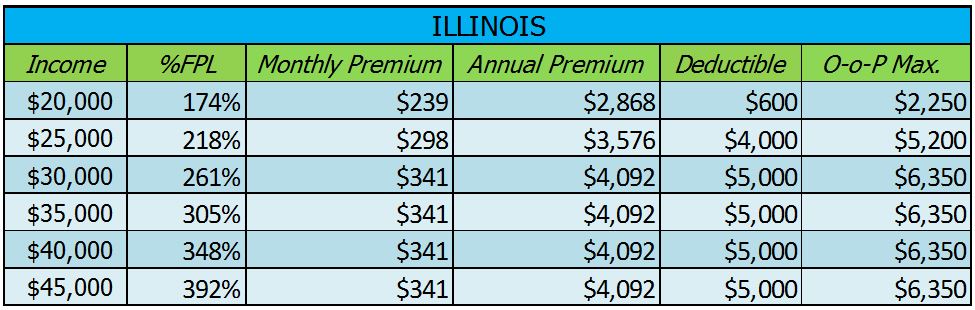

Forbes looked at four states: Arizona, Illinois, Pennsylvania, and Texas. Then they looked at a typical 30-year-old at one of six different annual income brackets: $20,000 in annual income, $25K, $30K, $35K, $40K, and $45K. Then for each of the four states, they computed how much an Aetna AET +0.25% Classic Silver plan would cost the same 30-year-old at each of these six income bands. They looked at monthly premiums, deductibles, and out of pocket limits.

If you look at the numbers, you’ll see why so many Millennials have Obamacare sticker shock. Someone earning $25K annually in Arizona will pay $2,424 in total monthly premiums for Obamacare (that’s 10% of their annual income!) and they’ll still get stuck with a $4,000 deductible and a $5,200 cap on their out of pocket costs. The same person in Illinois will pay $3,576 in annual premiums, and in Texas $2,460.

What about the same 30 year old who now earns $30,000 annually? This is the average salary for a pre-school teacher according to census data. In Arizona, their annual cost for carrying the Obamacare plan runs $2,772 and their deductible is $5,000. In Illinois, that same person will spend $4,092 for the same health plan, and also have a $5,000 deductible before their full health coverage kicks in.

Even someone earning $20K a year (the average salary for a full-time cashier) and eligible for Obamacare’s rich “cost sharing subsidies” is still going to find coverage pricey. In Pennsylvania, which was the lowest cost of the four states, the annual premium will run $1,620 for a plan that still leaves them with a $600 deductible. In Illinois, that same plan will cost $2,868 annually with the same $600 deductible. Premiums alone will eat up a whopping 14% of their annual income.

The health plans intentionally keep prices higher for young adults to subsidize older beneficiaries. Now, the White House is wringing its collective hands that the pool of applicants is skewing to older Americans. But this demographic distortion shouldn’t come as a surprise. It begs the question whether anyone in Washington did any market research before they launched this scheme, to see whether Millennials would show up?

Any wonder why patients are in love with our subscription model? For about $600 per year, they can see a doctor as often as they want, and pay nothing.